PSU’s Fiscal Plight

A reframing with real solutions

When Portland State University administrators speak of their current financial crisis, they focus all attention on the operational budget known as the Education and General Fund, or E&G. They do not speak of the institution’s total assets and income streams, its three reserve funds, or remedies that build sustainability by bringing the dwindling student enrollment numbers up. Instead, they are pursuing a corporatist strategy that pits mission against survival and infrastructure against educators.

Selective disclosure of institutional wealth and gap-closing options forecloses paths rather than opening them. By presenting PSU's fiscal challenges as an E&G shortfall only, the administration conceals its preordained conclusions about how it intends to move forward.

Following the lead of some of their peers who have also faced declining state support, PSU has decided to reorganize around market logic: faculty are pressured to generate revenue on a per-class basis, administrative structures expand to manage external partnerships, and programs whose value is civic rather than commercial are reclassified as liabilities.

Scholars call this reorganization “academic capitalism”. Writing in the 1990s, Sheila Slaughter and Larry Leslie documented this transformation in Academic Capitalism: Politics, Policies, and the Entrepreneurial University, a comparative study of public universities in the United States, Australia, Canada, and the United Kingdom.

A few years later, Slaughter and Gary Rhoades extended that analysis in Academic Capitalism and the New Economy, arguing that universities had come to treat knowledge not as a public good but as a commodity to be capitalized upon in profit-oriented activities. The university was not simply adapting to market conditions. It was actively reorienting its priorities, hiring patterns, and organizational structures to align with market criteria.1

The core argument of academic capitalism is that institutional harm need not involve bad actors. The theory explains why universities reward revenue-generating activity and abandon programs whose value cannot be measured in dollars. Programs that serve community members, working families, and first-generation students, whose value is civic rather than commercial, become problems to be solved rather than students to be served.

PSU’s invocation of a program-elimination framework, the Plan for Institutional Vitality and Organizational Transformation, or PIVOT, is academic capitalism with Oregon branding.

Academic Capitalism at PSU

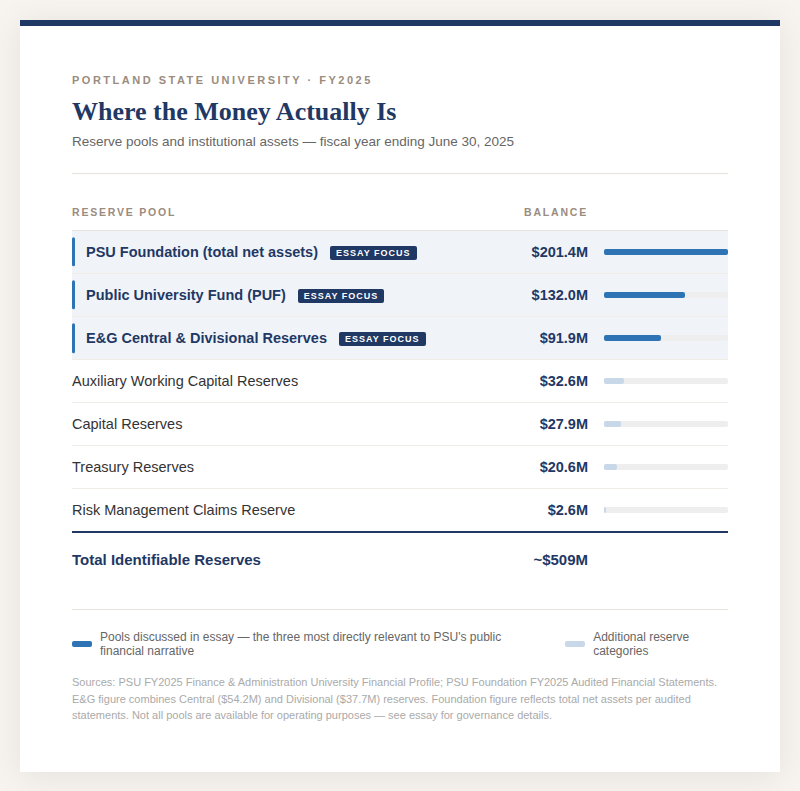

PSU is not a university without resources. It is a university with roughly $509 million in institutional assets across multiple reserve funds, one of which is being drawn down to cover an annual deficit in operational finances that has plagued the university since 2022. While the E&G gap of $40 million is real, the remedy administrators prescribe is not the only solution, or even the best one.

PSU’s administrative expansion, for instance, is a case in point. Growing the administrative branch of a university is a counterintuitive way to manage a shortfall because its impact has led to costs that run counter to the university’s mission. Nevertheless, an evaluation in 2024 by the Higher Education Coordinating Commission (HECC) documented that the annual growth rate in PSU’s spending on administration. It tracked institutional support, covering functions such as executive offices, legal, financial, accounting, space management, procurement, and information technology, and found that the sum of these expenditures was twice the total operating expenses during the same period when student enrollment declined.2

The proportion of total spending directed toward administrative functions grew from 7.1 percent to 9.5 percent. PSU built administrative capacity as its student population declined. The university’s per-student spending on administration doubled.

A rational management plan would begin reversing this costly trend, not only to save money but also to preserve academic programs that are core to the university’s mission. Under PSU’s current system, programs that earn more than they cost generate surpluses that subsidize administrative bloat. If they do not make a healthy profit, these programs are targeted for elimination.

Under academic capitalism, administrative growth is not a side effect. It is the mechanism by which the university remakes itself. Faculty must produce revenue, programs must cater to perceived market demand, and administrators multiply to manage market relationships, external partnerships, compliance functions, and strategic positioning. Those administrators require support staff. Support staff requires infrastructure. The costs accumulate at the center while the cuts land at the margins, and the margins at PSU are the programs serving the students least likely to appear in rankings or research metrics. PSU provides a case study of this model.

Collateral Damage

Programs that generate positive contribution margins (revenue above instructional cost) may appear on PIVOT elimination lists if they fall below PSU’s opaquely chosen threshold of 77 percent profit. That threshold represents the level at which a program is deemed to contribute sufficiently to university-wide overhead. That list includes administrative costs, facilities, technology, and institutional support. Courses and whole departments are judged not on academic value or even whether they lose money. They are held to a minimum profit standard to support PSU overhead.

As an example, the Postsecondary, Adult, and Continuing Education Program (PACE) has been classified for “sunset” even though it generates a 47 percent profit.3 A rational management plan retains programs that earn more than they cost, particularly when they serve a vital community need. PACE meets those standards. Its elimination is not a financial decision; it is a values decision. PACE serves working adults pursuing graduate credentials in education, counseling, and related fields. It aligns with Oregon’s documented workforce needs. PACE does not merely break even; it generates revenue, though not at the voracious profit mark that administrative bloat depends on.

The appearance of PACE on a PIVOT elimination list reveals a priority value not publicly stated: adult learners do not fit the enrollment profile, the marketing model, or the revenue trajectory that academic capitalism prizes. They are workers. Many hold union cards. Many are the children of immigrants or of working-class families who did not have the opportunity to complete a degree when they were young. The PACE program exists because Oregon made a public commitment, decades ago, that the state’s urban research university would serve those students alongside the traditional-age undergraduates who generate more predictable tuition streams. It would seem, however, that PSU is retreating from that public commitment.

PSU’s Actual Financial Picture

Portland State University’s narrative is that it is broke. This narrative supports the institution’s rationale for threatening more than 200 employees’ jobs. It is the premise behind the proposed sunset of programs that serve working adults, first-generation students, and Oregon’s workforce. The cuts prompted by the E&G deficit, we are told, are inevitable, and there is no alternative.

This narrative fails to mention the academic capitalism philosophy underlying the advertised approach, and it omits a discussion of other alternatives. A full disclosure would include the university's complete financial picture.

PSU does not have a single pot of money; it has three. Each is governed by separate policies, legal structures, and rules about use. Together, those three sources amount to roughly $509 million in institutional assets, including multiple reserves.4 And this is in addition to revenue streams, such as state funding and tuition. Understanding what these resources are and how they work is essential for any meaningful conversation about what is being done to Oregon’s urban public university and who is being asked to bear the pain.

The First Pot: The Public University Fund

Portland State has invested approximately $132 million in the Oregon Public University Fund (PUF). It is not endowment money. It is not donor money. It is PSU’s own operating cash, fed by tuition revenue, state appropriations, and other institutional income, held with the Oregon State Treasury for investment until needed for operations.

The PUF is an investment reserve established by the 2014 Oregon Legislature and administered by Oregon State University on behalf of five participating public universities, including Eastern Oregon University, Oregon Institute of Technology, Southern Oregon University, Western Oregon University, and PSU. The Treasury invests participant funds in intermediate-term fixed income securities under the governance of the Oregon Investment Council, held to strict benchmarks. In fiscal year 2025, PSU’s share of the PUF earned $6.6 million. As of June 30, 2025, PSU’s share of the fund made it the single largest participant in the pool’s total assets of $250 million.

The PUF is separate from, and in addition to, the Education and General fund reserves discussed in Board of Trustees meetings. The PUF is where PSU’s cash sits while invested with the Oregon State Treasury; the E&G reserves are the accounting category that tracks institutional cash remaining available. This is not the same money counted twice. When administrators speak of reserves, however, they speak only of the E&G balance. They do not mention the PUF. This omission is worth noting.

The Second Pot: The E&G Reserves

The Education and General fund reserve is the operating cushion PSU has built over the years when revenues exceeded expenditures. As of fiscal year 2024, those reserves stood at approximately $97 million, and PSU has been drawing them down at a rate of $17 to $18 million per year, spending more than it takes in every year since 2022.

The PSU Board of Trustees adopted a Reserves Management Policy in 2016, establishing a mandatory floor. Reserves must cover at least 90 days of operating expenses. The university has already breached that threshold. The Board approved the use of $18 million in reserves for fiscal year 2025, explicitly acknowledging the breach. At this spending rate, the HECC’s 2024 university evaluation estimates that the E&G fund will be exhausted in less than four years. PSU has a deficit. No one disputes it. What is disputed is the claim that this aspect tells the whole story.

The Third Pot: The PSU Foundation

The Portland State University Foundation held $201 million in net assets as of June 30, 2025, accumulated through donor gifts, endowments, bequests, and fundraising proceeds. Of that total, $185.4 million is donor-restricted, meaning it is legally bound to purposes designated by donors and is unavailable to cover general operating deficits. The $15.6 million, however, is unrestricted.5 The Foundation is a legally separate entity, governed by its own Board of Trustees and bound by state laws governing institutional funds. Endowed funds are subject to legal restrictions tied to donor intent. The Foundation cannot be redirected to cover operating deficits, and the university cannot access its assets without satisfying those donor restrictions and Foundation governance requirements.

The Foundation’s annual spending distribution, typically four to five percent of market value, flows back to the university for donor-designated purposes: scholarships, named faculty chairs, and specific academic programs. It supplements the university’s academic mission. It does not and cannot replace state appropriations or tuition revenue. The Foundation’s $201 million exists; it is part of PSU’s total institutional wealth, and no complete accounting of PSU’s financial condition omits it.

A Combination of Solutions is Called for

To forge a path forward that is better aligned with PSU’s mission and values as an Urban Research University, a blend of revenue and expense remedies is imperative – one that makes educator losses an option of last resort.

Here is a list of actions that could preserve the university, return it to a sustainable, thriving campus, and retain most of the people whose contributions turn mission into accomplishment:

1. Enrollment Revitalization

Because years of enrollment decline have made sustainability a fragile goal, job number one is to reverse this 10-year trend. PSU simply cannot resolve an enrollment-driven revenue crisis without a funded enrollment strategy. The Board of Trustees should require a specific, resourced plan for enrollment recovery, including a transparent accounting of current enrollment management expenditures across all funds and incorporating a multi-year target for student growth.

Additionally, PSU-AAUP President Bill Knight has argued publicly that the university should direct its energy toward recruitment, retention, and growth rather than cuts. Among the top 50 metro areas in the United States, Portland is a stark outlier in the percentage of its population enrolled in public four-year institutions, meaning PSU has an untapped market, not an exhausted one.6 Knight has called for strengthening direct pipelines with Portland Public Schools and Portland Community College, establishing direct billing agreements with major Oregon employers, and mobilizing the city of Portland as a partner in the university’s future.

It will never be true that contracting academic offerings will entice more students to PSU; only retention and, perhaps, expansion, can do that.

2. Cut Administrative Bloat

A second urgent and obvious strategy is to pare back the excessive layer of administration and overhead—fully 17 percent of the current budget goes to administration and the president’s office alone.

3. Boost Revenue

For the 2026-27 academic year, the University of Oregon is raising tuition by 4.5 percent.7 Oregon State University is proposing a 4.97 percent hike.8 A modest 2 percent tuition increase at PSU would keep student costs lower than those at OSU and UO, yet still yield $3 to $4 million while potentially attracting students who can no longer afford the other two.9 A modest increase is unlikely to have a deleterious impact on enrollment, particularly when compared to canceling courses, programs, and whole departments.

4. Revisit Institutional Options

There are several pieces to this strategy. First, a truth-in-advertising approach is vital. Budget communications to the Board, public officials, the campus community, and the public should clearly distinguish between rising per-student costs driven by enrollment declines and those driven by expansion. Conflating the two produces inaccurate institutional narratives and misdirects reform efforts.

Next, programs with demonstrated positive contribution margins should be retained unless the university can prove that their elimination would improve, rather than worsen, PSU’s net financial position.

Third, the Board should consider its net worth the way any business or household would. The Public University Fund (PUF) was established precisely for use in a moment like this. Its 2025 income generation of $6.6 million—already flowing into the operating revenue pot – is not its only value. A one-time strategic withdrawal from the PUF principal would bridge the remaining structural gap without touching other reserves and with minimal impact to the investment corpus.

Some might object to this latter action as eating PSU’s seed corn. While dipping into restricted Foundation resources would surely be anathema to sound legal and fiscal management, the PUF is a different matter entirely. It is not an endowment, but rather, PSU’s own operating cash. If tuition and state resources can be deposited, they can also be withdrawn. Though PSU board policy constrains this option in its Reserves Management Policy, it can also amend it—and it should.

Together, reducing administrative overhead, increasing enrollment, boosting revenue, and closing the remaining gap with PUF resources can build a sustainable path forward.

The Board of Trustees Reserves Management Policy, the PUF investment statements, the HECC university evaluation, and the PSU Foundation’s audited financial statements are all public documents, available to any Oregonian who chooses to look. None of them support the narrative that Portland State faces a crisis so acute that programs serving working Oregonians must be eliminated while administrative spending grows. Portland State is not out of money. It is not out of solutions.

It is out of alignment with its founding purpose, but it’s not too late to change course.

Sheila Slaughter and Larry Leslie, Academic Capitalism: Politics, Policies, and the Entrepreneurial University (Baltimore: Johns Hopkins University Press, 1997); Sheila Slaughter and Gary Rhoades, Academic Capitalism and the New Economy (Baltimore: Johns Hopkins University Press, 2004).

Higher Education Coordinating Commission, University Evaluation: Portland State University, 2024. Available at hecc.oregon.gov.

The PACE program's 47 percent contribution margin is derived from Gray Associates institutional data reviewed by the author in his capacity as PACE Program Coordinator. Gray Associates (Gray DI) is the third-party data analytics firm engaged by PSU to generate instructional cost and revenue data for the PIVOT classification process.

Portland State University's PUF balance ($132 million), E&G reserves ($97 million), Foundation net assets ($201 million), and PUF investment earnings ($6.6 million for FY2025) are reported in Andria Johnson, 2024-25 University Financial Profile, presented to the PSU Finance, Administration and Audit Committee, January 29, 2026, and in PSU's 2024-25 Audited Financial Statements, reviewed at the same meeting. The PUF is administered by Oregon State University on behalf of five participating public universities under the governance of the Oregon Investment Council. Docket, including audited financial statements, available at pdx.edu/board/finance-and-administration-committee.

Portland State University Foundation, Consolidated Financial Statements, fiscal year ended June 30, 2025, audited by Baker Tilly US, LLP, audit opinion dated October 31, 2025. The Consolidated Statement of Financial Position reports total net assets of $201,411,538, comprising $185,805,504 in net assets with donor restrictions and $15,606,034 in net assets without donor restrictions. Per Note 3 of the financial statements, net assets without donor restrictions represent resources “not subject to donor-restrictions and over which the Trustees of the Foundation retain control to use the funds in order to achieve the Foundation’s purpose and enhance University operations.” Available at psuf.org/Financials.

Bill Knight, PSU-AAUP President, public comment before the PSU Board of Trustees, January 29, 2026. Knight described Portland as a “shocking outlier” among the top 50 metropolitan areas in the percentage of population enrolled at public four-year institutions, and called for direct recruiting agreements with Portland Public Schools and Portland Community College.

University of Oregon Board of Trustees, tuition resolution for the 2026-27 academic year, approved March 17, 2026. In-state undergraduate tuition increased 4.5 percent for incoming students. Available at lookouteugene-springfield.com.

Oregon State University Board of Trustees, tuition resolution for the 2026-27 academic year, approved March 14, 2026. The weighted average increase for Oregon resident undergraduates was 4.97 percent; continuing undergraduates faced a 5.75 percent increase. Available at news.oregonstate.edu.

Revenue estimate derived from Vice President for Finance and Administration Andria Johnson's tuition recommendation memorandum to President Ann Cudd, dated March 25, 2025, and presented to the Finance, Administration, and Audit Committee of the Board of Trustees on April 3, 2025. The memo states that a 5 percent tuition increase would generate approximately $5 to $6 million in net revenue against a projected $17.8 million E&G gap, implying a per-percentage-point yield of roughly $1.6 to $2 million. The document is publicly available in the April 3, 2025, docket of the Finance, Administration and Audit Committee at pdx.edu/board/finance-and-administration-committee.

Very thorough analysis. Thanx! C2

Wow, I taught there a few years and spoke to many classes there over about 20 years.

Im pretty sure everything I taught would be considered "civic".

Sounds like the end of critical thinking, everything with the word "Justice" in it.

This is both sick an sad.

Are we bowing down to everyone working on slave wages and dumping down our future generations?

Not okay